The Ultimate Guide to Real Estate Tax Benefits for W-2 Income Earners

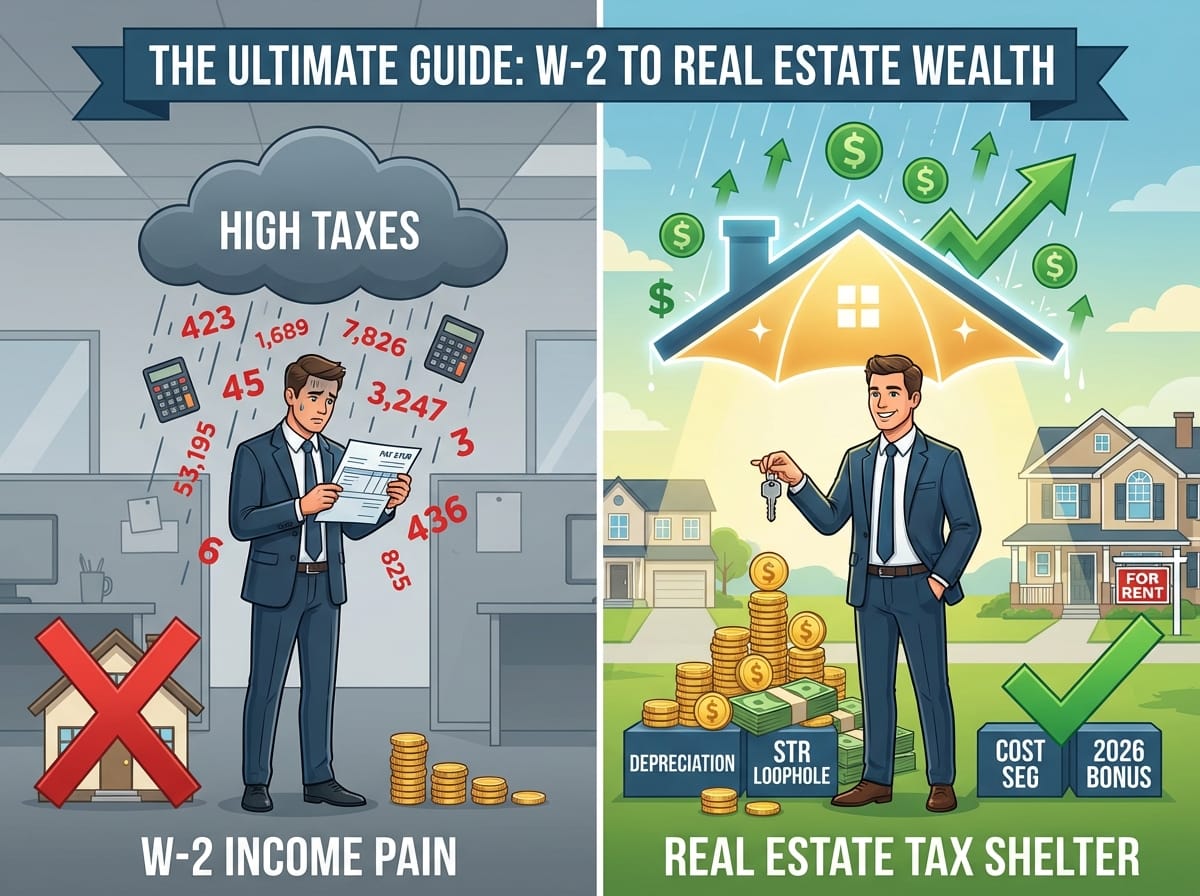

If you are a high-earning W-2 employee, you likely feel the pain of a high tax bill every time you look at your pay stub. Unlike business owners, W-2 earners have very few ways to reduce their taxable income. However, starting a real estate investing side hustle is widely considered one of the most powerful wealth-building tools available, largely because it acts as a legal tax shelter.

Many investors choose to invest in real estate as a strategic way to divert taxes from money earned from their day jobs. By understanding specific tax codes, you can legally use the losses from your real estate side hustle to offset your active W-2 income, keeping more of your hard-earned money in your pocket.

Real Estate as a Legal Tax Shelter: The Basic Deductions

Before diving into advanced strategies, it is important to understand the everyday tax advantages of owning rental property. Almost everything it takes to run your real estate business is tax-deductible. These deductions lower the net income of your property, which lowers the taxes you owe.

Common deductible business expenses include:

- Property Maintenance: Repairs, landscaping, and general upkeep.

- Carrying Costs: Property taxes, insurance, and utility expenses.

- Professional Fees: Commissions paid for real estate sales, purchases, and property management services.

- Business Operations: Office and home office space, along with basic office supply expenses.

- Travel: Mileage related to driving to your properties or managing your real estate business.

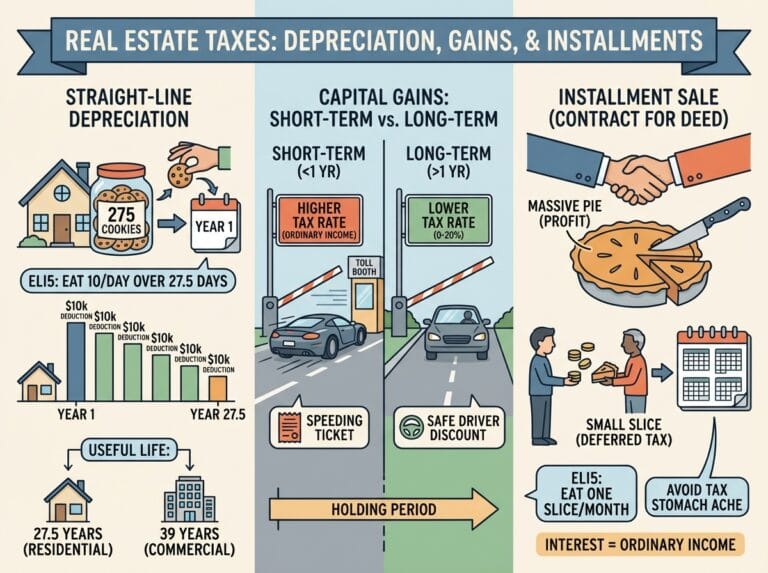

Demystifying Depreciation: The Real Estate Investor’s Best Friend

While writing off utilities and repairs is great, the true magic of real estate taxation lies in depreciation. The IRS recognizes that buildings degrade over time. Therefore, they allow you to deduct the cost of the building structures, plus any capital improvements, over a period of 27.5 years for residential property.

ELI5 (Explain Like I’m 5): What is Depreciation?

Imagine you buy a brand-new bicycle. Every year you ride it, the tires wear down, the paint chips, and it gets a little older. If you were to sell it after five years, it wouldn’t be worth what you paid for it. The IRS looks at a rental house the exact same way. They let you pretend the house is losing value every year and let you deduct that “loss” from your taxes. The secret superpower here is that, unlike the bicycle, real estate usually goes up in value in the real world, while you still get to claim the tax deduction for it wearing down!

Example: If you buy a rental property where the building itself (excluding the land) is valued at $275,000, you can divide that by 27.5 years. This gives you a $10,000 depreciation deduction every single year, regardless of whether the property goes up in market value.

The Passive Loss Rule Challenge

Here is where W-2 earners run into a wall. The IRS categorizes income into two main buckets: Active (your W-2 job) and Passive (rental properties). Normally, the IRS strictly states that passive losses can only offset passive income. If your rental property shows a paper loss of $15,000 due to depreciation, you generally cannot use that $15,000 to lower your W-2 tax bill.

To cross that barrier and use real estate losses against your W-2 income, you have to use one of two specific tax code exceptions.

Exception 1: Real Estate Professional Status (REPS)

The IRS allows you to offset your W-2 income with real estate losses if you qualify for Real Estate Professional Status. However, this is incredibly difficult for a full-time W-2 employee to achieve. To qualify, you must spend at least 750 hours a year in real estate activities, AND more than 50% of your total working hours must be in real estate.

If you work a standard 2,000-hour-a-year W-2 job, you would mathematically need to work over 2,001 hours in real estate to pass the 50% test. For most full-time employees, REPS is impossible.

Exception 2: The Short-Term Rental (STR) Loophole

Because REPS is out of reach for most, the Short-Term Rental (STR) Loophole is the golden ticket for W-2 income earners. According to the tax code, if the average stay of your tenants is seven days or less (think Airbnb or VRBO), the IRS does not consider it a “rental activity.” Instead, it is treated as an active business, like running a hotel.

Because it is an active business, you do not need to meet the impossible 50% rule of REPS. You simply need to achieve “Material Participation.” The easiest way to do this is to spend at least 100 hours managing the short-term rental and ensure no one else (like a property manager or cleaner) spends more time than you do.

ELI5: The STR Loophole

Think of the IRS as a strict school principal. The principal says kids in the “Passive Club” (long-term rentals) cannot sit at the same lunch table as kids in the “Active Club” (W-2 jobs). But, if you rent your property to guests for very short stays, the principal gives you a special pass. You are now officially in the “Active Club” and can share your snacks (tax deductions) across the table!

Supercharging Deductions: The Cost Segregation Study

If you want to create massive paper losses to offset your W-2 income using the STR loophole, standard depreciation (divided over 27.5 years) might not be fast enough. This is where a Cost Segregation Study comes in.

A cost segregation study is performed by a specialized engineer who walks through your property and identifies every single component that degrades faster than 27.5 years.

ELI5: Cost Segregation

Imagine buying a fully furnished dollhouse. Instead of saying the whole dollhouse takes 27 years to break, an expert comes in and says, “The wooden walls take 27 years, but the tiny carpets will wear out in 5 years, the tiny refrigerator will break in 5 years, and the little fences will last 15 years.”

By breaking the property down, you are allowed to accelerate the depreciation of the carpets, appliances, fixtures, and landscaping. Instead of taking tiny deductions over 27.5 years, you can take massive deductions in the first 5 to 15 years.

Bonus Depreciation: What Donald Trump’s Tax Law Means for 2026

Accelerating your depreciation is powerful, but it gets even better with Bonus Depreciation. Introduced under Donald Trump’s Tax Cuts and Jobs Act (TCJA) of 2017, bonus depreciation allowed investors to take 100% of the accelerated depreciation (the carpets, appliances, and fences from our dollhouse example) in the very first year of ownership.

However, the TCJA included a phase-out schedule for this benefit. It was 100% through 2022, and then began dropping by 20% each year.

For the tax year 2026, Bonus Depreciation is set at 20%.

While 20% might sound low compared to the 100% glory days of 2022, it is still a highly lucrative tool. Here is a real-world example of how it works in 2026 for a W-2 earner:

- You buy an Airbnb (Short-Term Rental) for $500,000 in 2026.

- You materially participate (work 100+ hours, more than anyone else).

- You order a Cost Segregation Study, which identifies $100,000 worth of 5-year and 15-year property (appliances, flooring, fixtures).

- Under the 2026 tax law, you can apply the 20% bonus depreciation directly to that $100,000. That gives you an immediate $20,000 deduction in year one.

- You also get standard depreciation on the remaining value of the home, plus all your standard deductions (taxes, insurance, utilities, repairs, mileage).

This easily creates a scenario where your property might generate positive cash flow in your bank account, but shows a $30,000 “loss” on paper. Thanks to the STR Loophole, you take that $30,000 loss and subtract it directly from your W-2 salary, saving you thousands of dollars in income taxes.