Unlocking Your Retirement: The IRA Withdrawal for First Time Home Buyers

Individual Retirement Accounts (IRAs) are powerful tools for building wealth. They offer fantastic tax benefits, such as tax-deductible contributions and tax-deferred investment gains. Because of these perks, the government wants you to keep that money saved for your golden years. To enforce this, IRAs are governed by strict rules that limit your access to the funds.

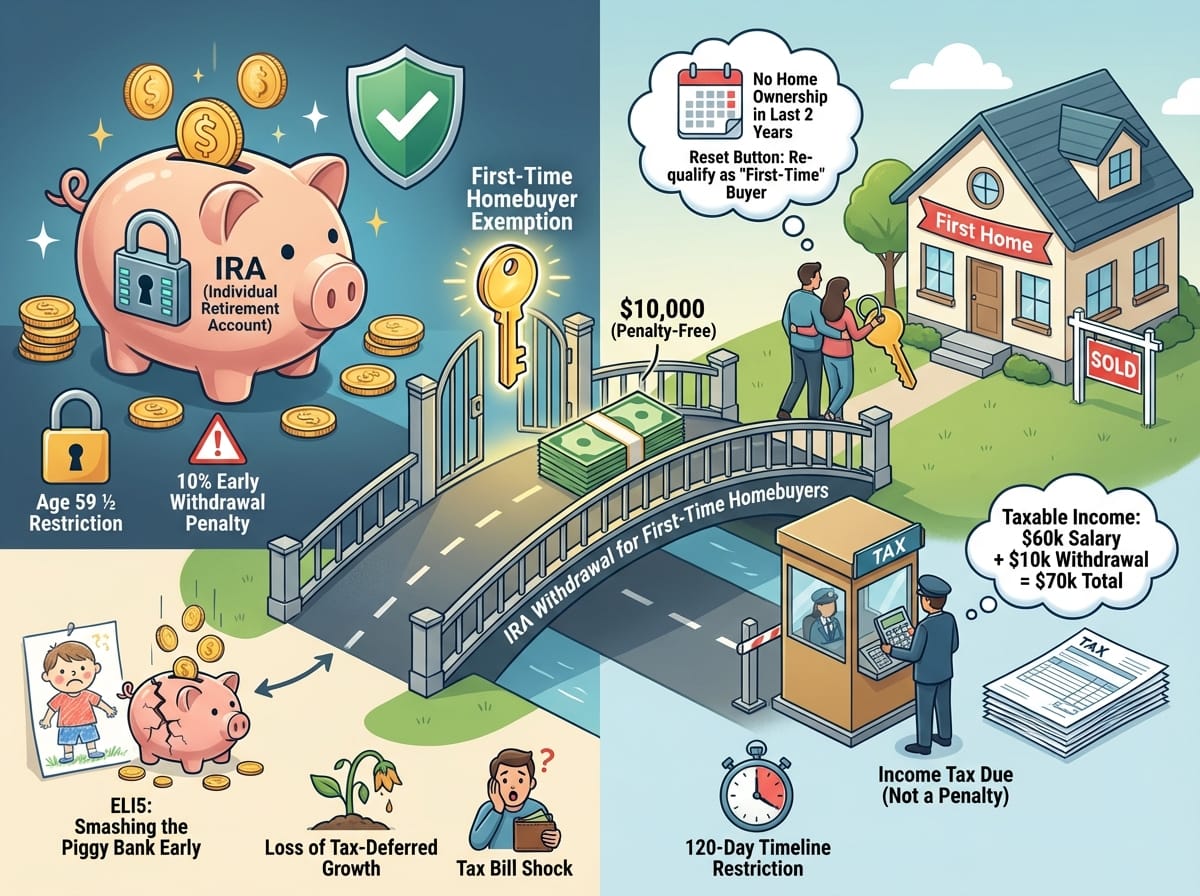

However, life happens, and buying a house is one of the biggest financial milestones you will ever face. If you are struggling to come up with a down payment, you might be looking at your retirement savings. Fortunately, the IRS provides a special loophole: the IRA withdrawal for first-time homebuyers.

The Golden Rule: The Age 59 ½ Restriction

Under standard Federal income tax laws, the IRS imposes a strict early withdrawal tax penalty on traditional IRAs. If you pull money out of your account before you reach the age of 59 ½, you are typically hit with a 10% early withdrawal penalty on top of any regular taxes you owe.

ELI5 (Explain Like I’m 5): Think of your IRA like a special piggy bank that has a built-in alarm. The government gave you free candy (tax breaks) to put your money inside, but the rule is you can’t open it until you are old. If you smash the piggy bank open before you turn 59 ½, the alarm goes off, and the government takes 10% of your money as a “rule-breaking fee.”

The First-Time Homebuyer Exemption

To help Americans achieve the dream of homeownership, the IRS created an exception to the early withdrawal penalty. A first-time homebuyer can withdraw up to $10,000 from their IRA to use as a down payment or to pay closing costs on a home—completely free of the 10% early withdrawal penalty.

What Actually Qualifies as a “First-Time” Homebuyer?

The IRS definition of a “first-time homebuyer” is much more forgiving than it sounds. You do not actually have to be purchasing a home for the very first time in your life.

To qualify, you (and your spouse, if you are married) simply must not have owned a principal residence at any time during the two years prior to the purchase date of the new home.

ELI5: Let’s say you bought a house ten years ago, sold it three years ago, and have been living in a rented apartment ever since. Because you haven’t owned a home in the last two years, the IRS hits the reset button. You are magically considered a “first-time” buyer again and can use the $10,000 IRA exception!

The $10,000 Lifetime Limit

It is crucial to understand that the $10,000 limit is a lifetime limit per person, not a per-house limit. Once you use this $10,000 penalty-free withdrawal, you can never use it again.

However, if you are married and both you and your spouse have separate IRAs, you can both pull $10,000 from your respective accounts. This allows a married couple to combine their exemptions for a total of $20,000 toward a down payment.

Taxes vs. Penalties: Catching the Fine Print

This is where many homebuyers make a costly mistake. It is absolutely vital to understand the difference between a penalty and an income tax.

Be aware that although the early withdrawal does not incur the 10% penalty, income tax will still have to be paid on the amount withdrawn. Because you received a tax deduction when you originally put the money into your Traditional IRA, the IRS expects to collect regular income taxes when the money comes out.

ELI5: The IRS is waving the 10% “rule-breaking fee” for smashing your piggy bank early. However, they still count the money you took out of the piggy bank as if it were a bonus on your paycheck at work. You still have to pay your normal, everyday taxes on that money.

Example Scenario: Buying a Home with IRA Funds

Let’s look at a practical example of how this impacts your wallet during tax season:

- The Situation: Mark earns $60,000 a year at his job. He finds a house he wants to buy but is short on his down payment. He decides to withdraw the maximum $10,000 from his Traditional IRA under the first-time homebuyer exemption.

- The Penalty: Because Mark qualifies as a first-time homebuyer, the IRS waives the $1,000 (10%) early withdrawal penalty. Mark saves $1,000!

- The Taxes: The $10,000 is added to Mark’s taxable income for the year. The IRS now taxes Mark as if he earned $70,000 ($60k salary + $10k IRA withdrawal). Depending on his tax bracket, Mark might owe an additional $2,200 in standard income taxes come April.

Is Using Your IRA for a Down Payment a Good Idea?

While the first-time homebuyer exception is a great fallback option, it should be carefully considered before taking action. Here are a few quick points to keep in mind:

- Loss of Tax-Deferred Growth: When you pull $10,000 out of your retirement account in your 30s, you aren’t just losing $10,000. You are losing decades of compound interest that the money would have earned by the time you retire.

- Tax Bill Shock: As shown in the example above, you must be prepared to pay the income taxes on the withdrawn amount at the end of the year. If you spend your entire withdrawal on the house, you might not have enough cash left over to pay Uncle Sam.

- Timeline Restrictions: Once you withdraw the funds from your IRA, you generally have 120 days to use the money to buy, build, or rebuild your home. If the house sale falls through and you miss this window, you could be hit with the 10% penalty anyway.

Final Thoughts on Funding Your First Home

An IRA withdrawal for first-time home buyers can be the exact bridge you need to cross from renting to owning. By allowing you to access up to $10,000 penalty-free, the IRS makes it easier to secure a down payment. Just remember to budget for the standard income taxes you will owe on the withdrawal, and work closely with a tax professional or financial advisor to ensure you follow the 120-day rule to the letter.