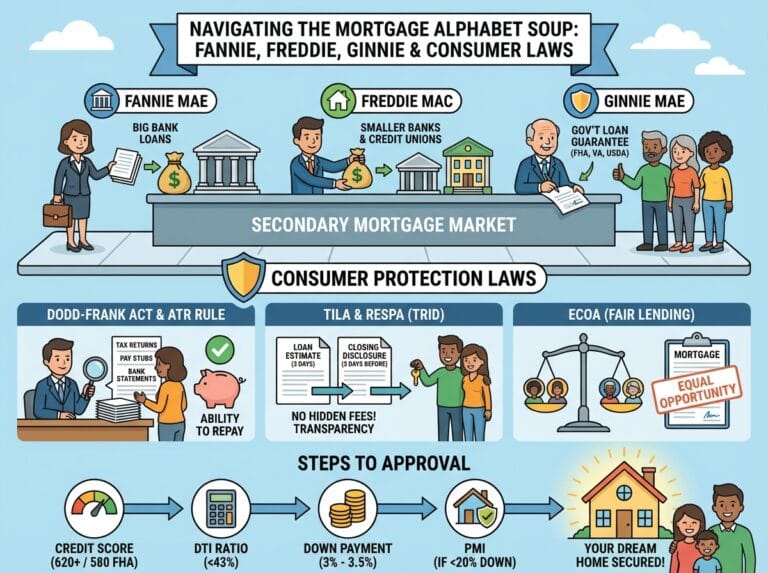

The 2008 financial crisis reshaped the landscape of American real estate. In response to the housing market crash, the federal government enacted the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010. For Florida real estate investors, buyers, and sellers, this legislation changed exactly how property transactions are handled, particularly regarding seller financing. Understanding the Dodd-Frank Act is essential for anyone looking to navigate the Florida housing market legally and profitably.

Understanding the Dodd-Frank Act

The Dodd-Frank Act is a massive piece of federal legislation designed to promote financial stability by improving accountability and transparency in the financial system. For the real estate sector, its primary goal is to protect consumers from predatory lending practices. It mandates that lenders must thoroughly verify a borrower’s ability to repay a loan before issuing a mortgage.

ELI5: The Dodd-Frank Act Explained Simply

Explain Like I’m 5 (ELI5): Imagine you and your friends are playing a game of Monopoly. In the past, the banker was handing out massive loans to players who had no properties and no money. When those players went bankrupt, the whole game broke down and ruined the fun for everyone. Dodd-Frank is like a new, strict rulebook that forces the banker to check every player’s pockets and income before giving them a loan. If the player cannot prove they can pay it back, they do not get the loan.

The Impact on Florida Real Estate Transactions

While standard bank mortgages are heavily regulated by this act, the most significant impact on everyday Florida residents and investors involves seller financing, also known as owner financing. In a seller-financed transaction, the seller acts as the bank. Before Dodd-Frank, Florida sellers could easily offer financing to buyers with bad credit, charge high interest rates, and include massive balloon payments. The act strictly limits these practices to protect Florida homebuyers.

The Ability-to-Repay (ATR) Rule

Under Dodd-Frank, anyone creating a mortgage must ensure the borrower has a reasonable ability to repay the loan. This means Florida sellers offering financing must document the buyer’s income, current debts, employment status, and credit history. You can no longer simply rely on a buyer’s word or a large down payment to justify the loan.

Strict Limits on Balloon Payments

Historically, many Florida real estate investors used balloon payments. They would offer low monthly payments for five years, followed by a massive lump-sum payment for the remaining balance. Dodd-Frank heavily restricts and, in many cases, outright bans balloon payments for seller-financed primary residences, ensuring buyers are not trapped in loans designed to force foreclosure.

Dodd-Frank Exemptions for Florida Sellers

The federal government recognizes that average homeowners are not massive Wall Street banks. Therefore, there are specific exemptions built into the Dodd-Frank Act that allow Florida property owners to offer seller financing without jumping through every single regulatory hoop. These exemptions are categorized by the number of properties sold per year.

The One-Property Exemption

If you are an individual homeowner in Florida selling a property, you can finance the sale for the buyer under the following strict conditions:

- Frequency: You can only do this for one property within a 12-month period.

- Ownership: You must own the property, and it must secure the loan.

- No Builders: You cannot be the contractor or builder who constructed the home in the ordinary course of business.

- Terms: The loan cannot have a balloon payment, and the interest rate must remain fixed for at least the first five years.

The Three-Property Exemption

For Florida real estate investors or landlords, the rules allow for up to three seller-financed transactions per year, but the requirements are slightly different:

- Frequency: You can finance up to three properties in a 12-month period.

- Ability to Repay: Unlike the one-property exemption, you must investigate and document the buyer’s ability to repay the loan.

- Terms: Balloon payments are still generally prohibited, and interest rates must be fixed for the first five years.

The Penalties for Violating Dodd-Frank in Florida

Ignoring federal lending laws carries severe financial and legal consequences. If a Florida real estate seller violates the Dodd-Frank Act, the buyer is granted incredible legal leverage. The buyer can sue for damages, demand a refund of all interest and fees paid, and force the seller to cover all attorney costs.

Real Estate Example: The Consequences of Breaking the Rules

Example: Consider a Florida investor named John. John owns four rental homes in Orlando and decides to sell all of them in a single year using owner financing. He bypasses the Dodd-Frank rules, fails to check the buyers’ incomes, and includes a mandatory balloon payment after three years.

Two years later, one of the buyers, Sarah, loses her job and stops paying. John tries to foreclose on the property. However, Sarah hires an attorney who discovers John violated the Dodd-Frank Act by exceeding the three-property limit and failing to prove Sarah’s ability to repay. The court rules in Sarah’s favor. John is blocked from foreclosing, is forced to refund Sarah all the interest she ever paid, and has to pay her attorney’s fees. John loses tens of thousands of dollars because he ignored federal lending regulations.

Best Practices for Florida Real Estate Investors

To safely navigate the Florida housing market while utilizing seller financing, property owners must adopt a compliance-first mindset. Structuring deals correctly from day one prevents catastrophic legal losses down the road.

Work with a Licensed Mortgage Loan Originator (MLO)

The safest way to offer seller financing in Florida without running afoul of Dodd-Frank is to hire a licensed Mortgage Loan Originator. An MLO acts as a compliant middleman. They will gather the buyer’s financial documents, verify their income, check their credit, and ensure the loan structure meets all federal and state guidelines. Paying an MLO a modest fee protects the seller from severe federal penalties and ensures the transaction is completely legal.

Utilize Proper Documentation and Servicing

Always use official, state-approved promissory notes and mortgages. Furthermore, investors should use a licensed third-party loan servicing company to collect monthly payments, manage property tax escrows, and keep official records. A professional paper trail is the best defense against any future claims regarding lending violations.