A Comprehensive Guide to Real Estate Taxes: Straight-Line Depreciation, Capital Gains, and Installment Sales

Navigating the tax implications of real estate investing can feel overwhelming. From understanding how the IRS calculates wear and tear on your property to knowing how much you will owe when you sell, mastering these concepts is critical for maximizing your profits. In this guide, we will break down the straight-line depreciation method, the difference between short-term and long-term capital gains, and how you can defer taxes using an installment sale.

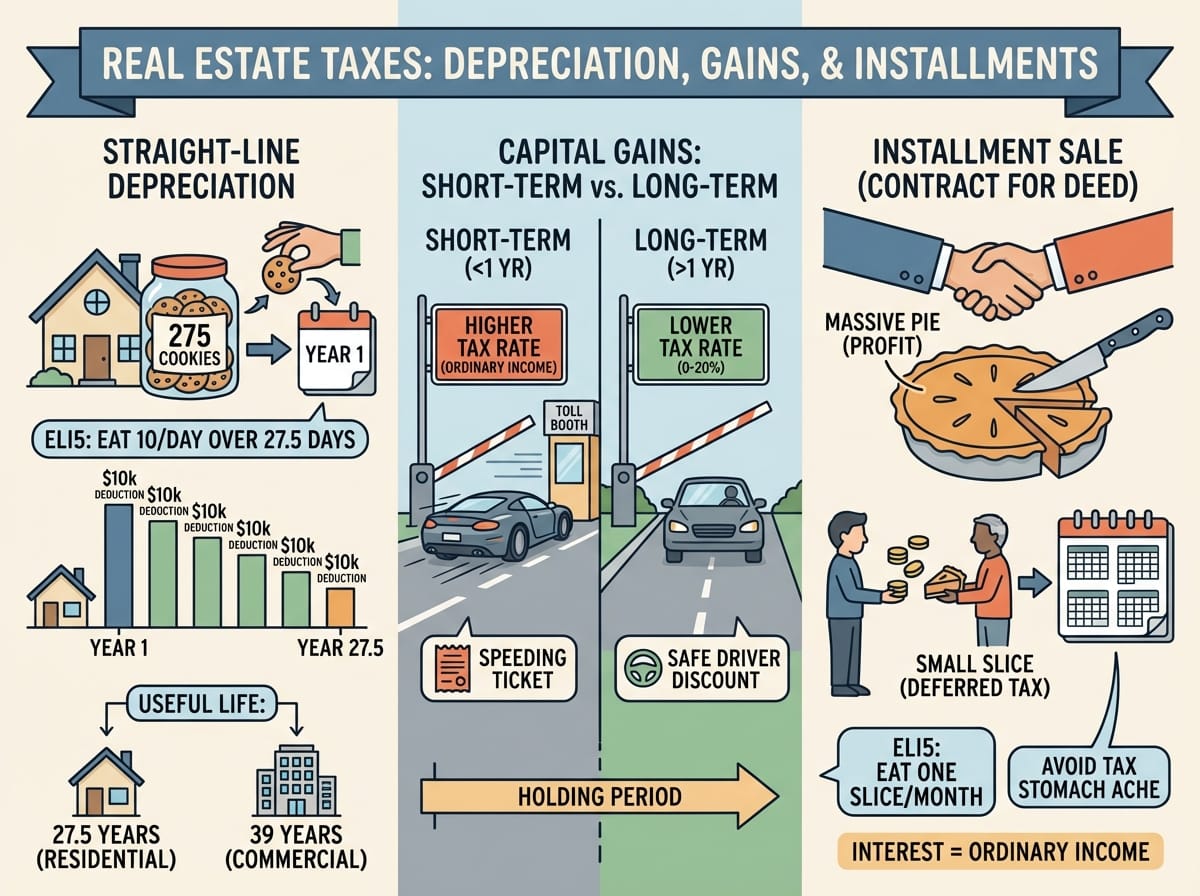

Understanding the Straight-Line Depreciation Method

When you purchase an investment property, the Internal Revenue Service (IRS) allows you to deduct the costs of buying and improving that property over its useful life. This reduces your taxable income each year. The most common way to calculate this deduction is the straight-line depreciation method.

What is Straight-Line Depreciation? (ELI5)

Explain Like I’m 5 (ELI5): Imagine you buy a giant pack of 275 cookies that has to last you exactly 27 and a half days. To make sure you do not run out, you eat exactly 10 cookies every single day. Straight-line depreciation works the same way. Instead of writing off the entire cost of a house on your taxes the year you buy it, the IRS makes you divide the cost evenly and take a small tax deduction every year for a set number of years.

The IRS “Useful Asset Life” Rules

The period over which you divide your depreciation is determined by the “useful asset life” of the property. The IRS has strict definitions for how long a property is considered useful:

- 27.5 Years: Residential rental property (like single-family homes, duplexes, or apartment buildings).

- 39 Years: Nonresidential income-producing property (like commercial office buildings or retail spaces).

Example: If you buy a residential rental property for $275,000 (excluding the value of the land, which cannot be depreciated), you would divide $275,000 by 27.5 years. This gives you a straight-line depreciation deduction of $10,000 every year to lower your tax bill.

Capital Gains Taxes: Short-Term vs. Long-Term

When you eventually sell your investment property for a profit, the IRS will tax that profit. This is known as a capital gains tax. The amount you pay depends heavily on exactly how long you owned the property before selling.

Short-Term Capital Gains

If you hold a property for one year or less before selling it, your profits are classified as short-term capital gains. The IRS treats short-term gains just like the regular salary you make at your job, meaning they are taxed as ordinary income.

For example, looking at the 2019 tax brackets, ordinary income tax rates ranged from 10% to 37% depending on your total income. If you fall into a high tax bracket, flipping a house quickly could result in a massive tax bill.

Long-Term Capital Gains

If you hold the property for longer than one year, you are rewarded with long-term capital gains tax rates. These rates are significantly lower than ordinary income tax rates. In 2019, the long-term capital gains tax rate was between 0% and 20%, depending on your normal income tax bracket.

Why Holding Property Longer Saves You Money (ELI5)

ELI5: Think of the IRS like a toll booth operator. If you drive through the toll booth really fast (buying and selling a house in under a year), the operator gives you a speeding ticket (a higher tax rate). If you drive slowly and wait more than a year to pass through, the operator gives you a “safe driver discount” (a much lower tax rate).

Example: You make a $50,000 profit on a house. If you flip it in 6 months and are in a 32% ordinary tax bracket, you pay $16,000 in taxes. If you wait 13 months to sell, you might only pay a 15% long-term capital gains rate, costing you just $7,500. You save $8,500 simply by waiting!

Delaying Taxes with the Installment Sale Method (Contract for Deed)

What if you want to sell your property but do not want to be hit with a massive capital gains tax bill all in one year? Investors can delay capital gains taxes by selling property through an Installment Sale, sometimes called a land contract or a contract for deed.

How an Installment Sale Works (ELI5)

ELI5: Imagine you bake a massive, delicious pie (your profit). If you eat the entire pie right now, you will get a terrible stomach ache (a huge tax bill). Instead, you decide to eat just one slice every month. An installment sale means you act like the bank. The buyer pays you a little bit every month instead of getting a mortgage. You only pay taxes on the small “slice” of profit you receive that specific year, preventing a tax stomach ache.

Because payments on the sale are taken over a period of years rather than in one single lump sum, federal income taxes are calculated only on the principal amount received in the year it is taxed. This can keep you in a lower tax bracket and make your tax burden much more manageable.

Reporting Interest on Installment Sales

When you act as the bank in an installment sale, you will naturally charge the buyer interest. It is vital to understand how the IRS views this interest.

- Taxed as Ordinary Income: While the principal portion of the buyer’s payment benefits from lower capital gains rates, the interest you collect is reported to the IRS as ordinary income.

- Mandatory Interest Rules: Even if you want to be nice and write an agreement with the buyer that says “zero interest,” the IRS does not allow this. The IRS will “impute” interest, meaning they will treat part of every payment as interest anyway.

- Down Payments: Generally, interest is not included in the buyer’s initial down payment. However, for every regular monthly payment that follows, a portion must be treated as interest.