Understanding the Capital Gains Tax Exclusion for Home Sellers

Selling your primary residence can yield a significant profit, and one of the best tax advantages available to property owners is the capital gains tax exclusion. If you meet specific criteria, the IRS allows you to exclude a massive portion of your profit from being taxed.

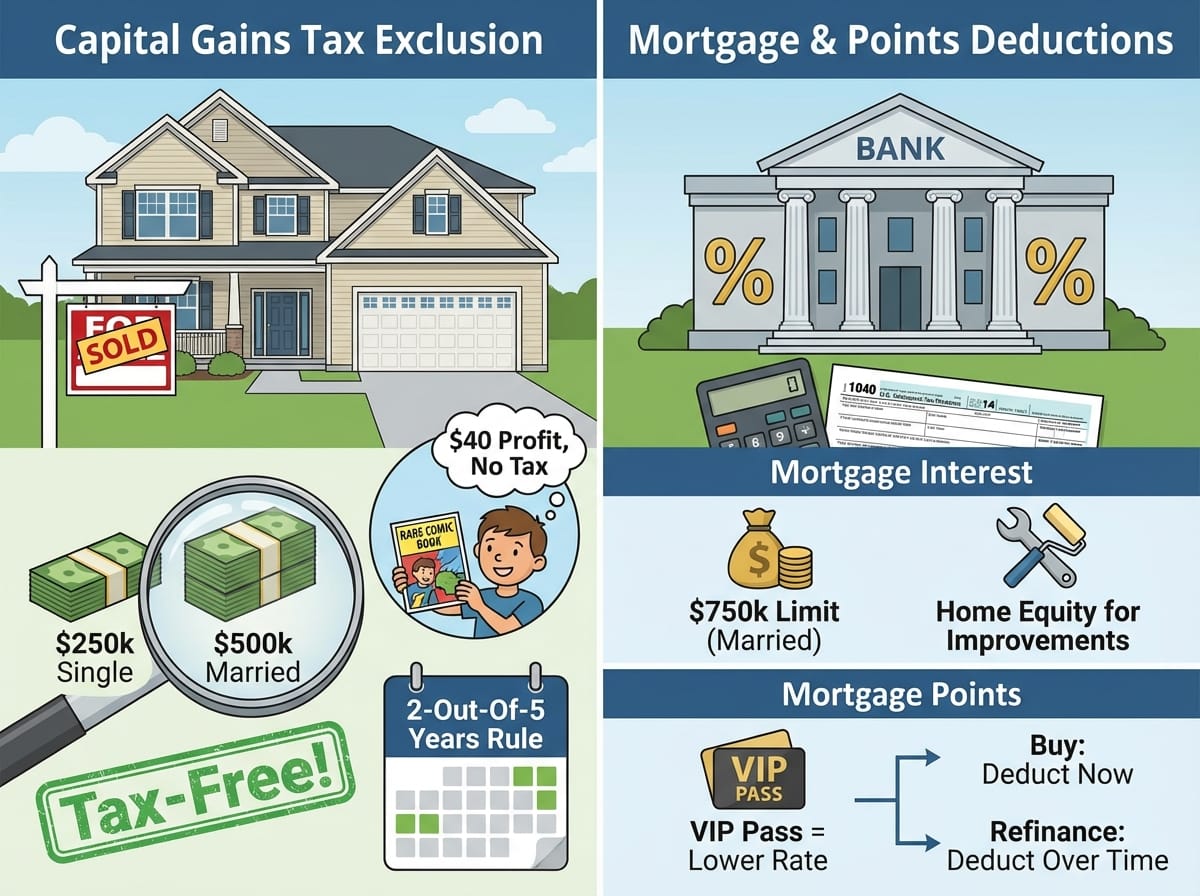

How the Exclusion Limits Work

When you sell a property for more than you paid for it, that profit is called a “capital gain.” For individual home sellers, the IRS allows an exclusion of up to $250,000 in capital gains. If you are married and filing jointly, that exclusion doubles to a generous $500,000.

ELI5 (Explain Like I’m 5): Imagine you buy a rare comic book for $10. A few years later, you sell it to a friend for $50. You made $40 in profit! Usually, the government wants a tiny slice of that $40 as a tax. But if that comic book was your absolute favorite and you kept it in your bedroom for a long time, the government says, “You can keep all $40, tax-free!” For adults, instead of a comic book, it’s their house, and instead of $40, they can keep hundreds of thousands of dollars tax-free.

Example: Let’s say a married couple bought a home for $300,000. Years later, they sell the home for $750,000. Their total profit (capital gain) is $450,000. Because they are married filing jointly and the profit is under the $500,000 limit, they will owe absolutely zero federal capital gains tax on that money.

The “Two-Out-Of-Five-Years” Rule

You cannot simply flip a house in six months and claim this tax break. To qualify for the capital gains exclusion, the homeowner must have resided in the property as their primary residence for at least two out of the five years immediately preceding the sale.

Example: Sarah buys a condo and lives in it from 2017 to 2019 (two full years). In 2020, she decides to travel and rents the condo out to tenants. In 2022, she sells the condo. Even though she wasn’t living there when she sold it, she meets the requirement because she lived in the property for two years within the five-year window prior to the sale date.

Maximizing Deductions on Mortgage and Home Equity Interest

Beyond selling your home, owning a property offers annual federal tax deductions. Understanding how to deduct the interest you pay to the bank can significantly lower your yearly tax bill.

The Tax Cuts and Jobs Act (TCJA) Mortgage Interest Limits

The Tax Cuts and Jobs Act (TCJA) revised the rules for mortgage interest tax deductions, effective for the 2018 tax year and beyond. The amount of mortgage debt eligible for an interest deduction was capped to reflect new federal standards.

- Married Couples Filing Jointly: Can deduct the interest paid on mortgage debt up to $750,000.

- Married Couples Filing Separately: Can deduct the interest paid on mortgage debt up to $375,000.

ELI5: When you borrow money from the bank to buy a house, the bank charges you a fee for borrowing that money. That fee is called “interest.” The government feels bad that you have to pay this fee, so they let you subtract it from your income at tax time. But, to make sure billionaires buying mansions don’t get too big of a break, the government put a ceiling on it. They will only give you a tax break on the interest for the first $750,000 you borrow.

Deducting Interest on Home Equity Loans

If you take out a home equity loan, you may also be able to deduct the interest paid on loan amounts between $50,000 and $100,000 under certain federal conditions. Generally, to qualify for this deduction today, the funds from the home equity loan must be used to “buy, build, or substantially improve” the home that secures the loan.

Example: David takes out a $60,000 home equity loan and uses the money to completely renovate his aging kitchen and add a new bathroom. Because he used the money to substantially improve his primary residence, he can deduct the interest paid on that $60,000 loan on his federal taxes.

How to Deduct Mortgage Points on Your Taxes

When you take out a mortgage or refinance an existing one, you might encounter “points.” A single point is equal to 1% of your total loan amount. The IRS offers specific rules for deducting these upfront costs.

Deducting Discount Points

Property owners may claim a federal tax deduction for discount points charged by home mortgage lenders. Discount points are essentially prepaid interest; you pay a lump sum upfront to lower your long-term interest rate.

ELI5: Imagine you are buying a VIP pass at an amusement park. You pay a big chunk of money right at the entrance gate, but in return, your lines for the rides are shorter for the rest of the day. Discount points are like that VIP pass. You pay the bank upfront, and in return, your monthly mortgage bill is smaller. The government lets you deduct the cost of that VIP pass on your taxes!

Deducting Origination Points When Refinancing

If you decide to refinance your home to get a better rate or change your loan terms, you might pay origination points. Unlike the points paid when you initially buy a home (which can often be deducted in full in the year you pay them), the IRS treats refinancing points differently.

Property owners may deduct origination points paid to refinance a home, but these points must be deducted gradually over the life of the loan.

Example: Mark refinances his mortgage into a new 30-year loan. To do so, he pays $3,000 in origination points. Instead of deducting the full $3,000 on his taxes this year, the IRS requires him to spread it out. He divides $3,000 by 30 years, meaning he will deduct $100 from his federal taxes every year for the next three decades.